Electric vehicles (EVs), including hybrids and plug-in hybrids, had a favourable financial treatment up until 1 April 2024. The clean car discount which was in place until 31 December 2023, and no road user charges (RUCs) before 1 April 2024, contributed to a sustained increase in the number of EVs on our roads over the last three years.

Electric vehicles (EVs), including hybrids and plug-in hybrids, had a favourable financial treatment up until 1 April 2024. The clean car discount which was in place until 31 December 2023, and no road user charges (RUCs) before 1 April 2024, contributed to a sustained increase in the number of EVs on our roads over the last three years.

However, their attraction from a financial perspective has now been reduced, which is reflected in the statistics from the March quarter of 2024 which show a flattening of the number of EVs on our roads after the previous sustained growth. (See graph)

For context, it is worth noting that as at 31 March 2024 , there are 5,781,885 registered vehicles in New Zealand, of which 3,634,925 are passenger cars/vans.

Introduction of road user charges for EVs

The RUC system was introduced in 1977 to help governments with paying for the cost of maintaining our roads. While petrol vehicles have a fuel tax levied at the pump, diesel has uses beyond public roads and therefore it is not appropriate to levy a roading tax at the point of purchase. The RUC system traditionally has applied to diesel vehicles and is levied based on distance travelled and vehicle type.

Initially, electric vehicles were exempted from paying RUCs as a way of encouraging the purchase of EVs in preference to new petrol or diesel vehicles. It was always intended that once the number of EVs reached 2% of the total light vehicle fleet, RUCs would be imposed on EVs. This target has now been met and thus the Government has discontinued the RUC exemption.

From 1 April 2024, fully electric vehicles are required to pay RUC of $76 per 1,000km and plug-in hybrids will pay at the rate of $38 per 1,000km (the lower amount reflects that some fuel excise duty is paid when petrol is purchased).

There is no doubt that this will increase the cost of running an EV. If the EV is a business vehicle, the extra costs should be a deductible expense (but may need to be apportioned for private use if the owner is a sole trader or for some small private companies).

Impact on employers

If you have company EVs that are provided to employees that are subject to FBT, nothing changes at this point – the same formula for calculating the FBT still applies.

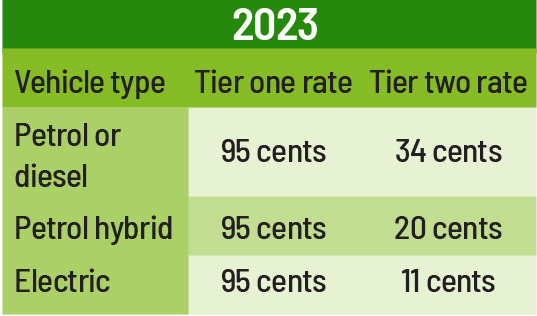

If you are reimbursing employees that use their own EVs for work travel, and use the Inland Revenue mileage rates to calculate the amount that can be paid tax-free, again at this stage nothing changes – the Inland Revenue mileage rates that were last refreshed in May 2023 still apply:

For more information on how the two tier reimbursement system works, please refer to our June 2023 Tax Alert article.

Typically, Inland Revenue issues mileage new rates around May/June each year, so we anticipate some new rates being released shortly. Remember that for reimbursements the new rates apply from the date that they are released, so you should be prepared to update systems and possibly the amount you reimburse to staff from that date.

The rates are intended to reflect the cost of running the different types of vehicles, so with the increase in the relative cost of running EVs, we would expect to see much less variance between the tier two rates in future. While it would be a welcome taxpayer-friendly concession, there may not be enough of an increase in running costs to warrant a single tier two rate for all vehicle types.

If this all sounds quite complex, please seek assistance from your accountant or tax adviser.

Related: Tax changes taking effect this month